Hundi-Tantra: Credit Transfer Across Continents

Shroffs and Sahukars - The SWIFT of the Ancient World

How Indian merchants invented the world's first international payment system, the hundi, enabling value transfer across continents without moving a single coin, principles that live on in modern UPI and digital payments.

The Problem of Heavy Money

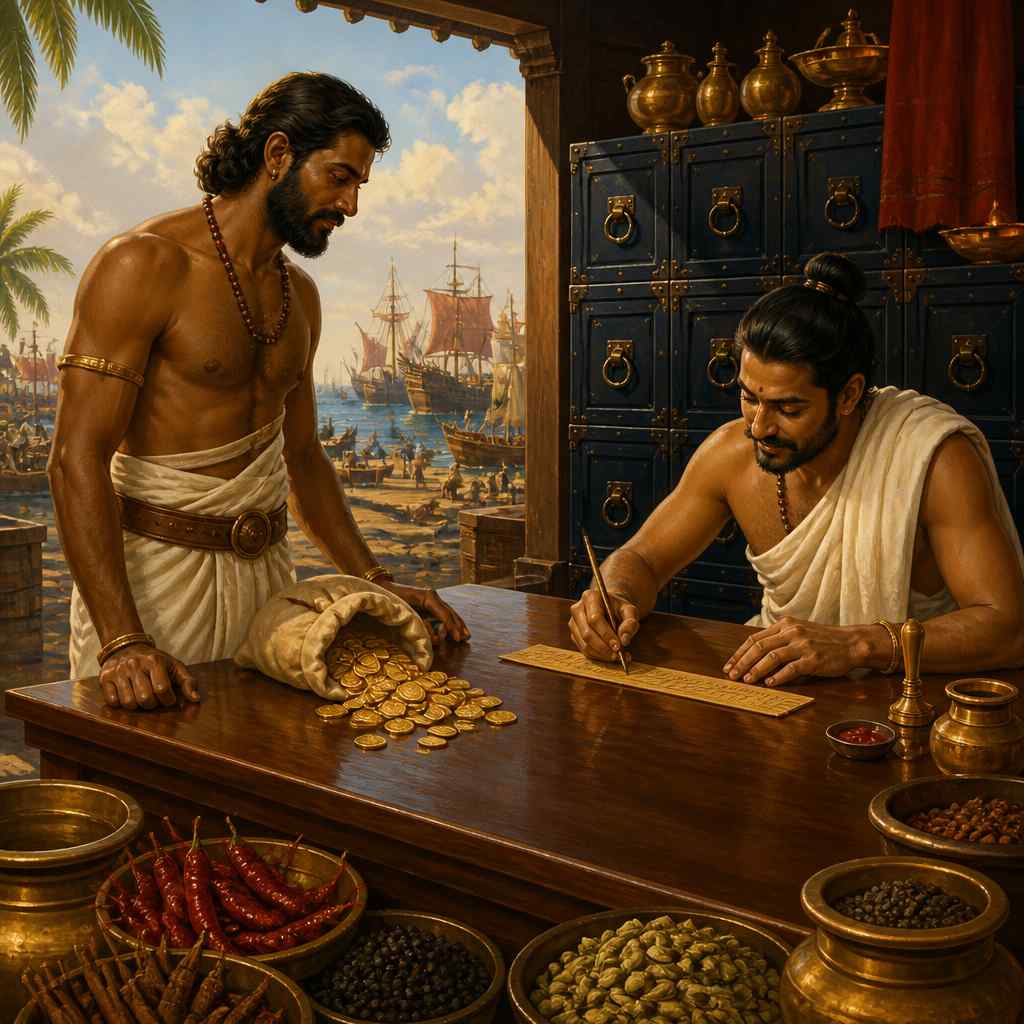

Chandragupta, a spice merchant from Muziris (modern Kerala), faced a problem that every long-distance trader knew. He needed to buy pepper, thousands of bags, but carrying the payment was nearly impossible.

The Romans paid in gold. Beautiful, heavy gold. Carrying 10,000 denarii worth of gold from the coast to the pepper gardens in the Western Ghats meant:

- Weight: Hundreds of kilograms of metal

- Risk: Bandits knew the trade routes

- Time: Slow caravans, armed guards, fortified camps

- Cost: Guards, storage, transport, all eating into margins

The alternative was worse: leaving gold at the port meant trusting warehouses and strangers.

But Chandragupta had another option. He visited his shroff (banker) at the port. The shroff examined his gold, weighed it, tested its purity. Then he wrote a document, a hundi (हुण्डी), authorizing his correspondent in the hills to pay Chandragupta the equivalent in local currency.

Chandragupta walked out carrying a small piece of cloth. No gold. No guards. No risk. Three weeks later, in the pepper country, he presented the hundi to the correspondent shroff. The shroff verified the seal, checked his ledgers, and paid out in full.

Value had moved 200 kilometers without moving at all.

What Made Hundis Revolutionary

The hundi was a negotiable credit instrument, essentially a bill of exchange or banker's draft. But its sophistication exceeded anything the ancient world had seen.

A typical hundi included:

- Drawer: The person creating the hundi (issuing shroff)

- Drawee: The person who would pay (correspondent shroff)

- Payee: The person who would receive payment (merchant)

- Amount: Specified in a standard currency or weight

- Date: When payment was due (some were payable on sight, others on fixed dates)

- Conditions: Any specific terms (e.g., "to bearer," "to named payee only")

The genius was in the network. Hundis worked because shroffs across vast distances trusted each other. A shroff in Muziris could issue a hundi payable in Mathura, 1,500 kilometers away, because shroffs in both cities belonged to interlocking trust networks.

"हुण्डी-प्रमाणेन धनं प्राप्यते।" "By the authority of the hundi, wealth is obtained." , Commercial maxim

This wasn't just convenience, it was a financial technology that enabled trade on a scale otherwise impossible.

Types of Hundis

The hundi system developed remarkable sophistication, with different instruments for different purposes:

Darshani Hundi (Sight Draft): Payable immediately upon presentation. Used for urgent payments where the payee needed funds right away.

Muddati Hundi (Usance Draft): Payable after a specified period (30 days, 60 days, etc.). This built in credit, the payee could use goods immediately while payment followed later.

Shah-jog Hundi: Payable only to a respectable person ("shah"), essentially requiring the payee to prove their identity and standing. Security through social verification.

Dhani-jog Hundi: Payable to the holder. Fully negotiable, could be traded, sold, or used as payment. The most liquid form.

Jokhmi Hundi: A trade-contingent draft, payment was conditional on goods arriving safely. Combined bill of exchange with insurance. If the ship sank, no payment was due. If goods arrived, payment triggered.

This variety shows how Indian merchants had thought through virtually every commercial scenario and created appropriate instruments.

The Shroff Network

Hundis worked because of the shroff (from Sanskrit shreshtha, "best"), the banker-money-changer who formed the backbone of India's financial system.

Shroff functions included:

Money Exchange: Converting between currencies (Roman, Persian, Chinese, local) at known rates.

Hundi Issuance: Creating credit instruments payable at distant locations through correspondent relationships.

Deposit Banking: Accepting deposits and paying interest, sometimes higher than modern banks offer.

Trade Finance: Providing credit to merchants for purchasing inventory.

Assaying: Verifying precious metal purity, essential when coins from different empires circulated.

Shroffs operated through family networks. A shroff house in Surat might have branches (or allied houses) in Lahore, Delhi, Calcutta, and even Samarkand or Baghdad. Funds could move anywhere the network reached.

"श्रेष्ठी-गृहे निक्षिप्तं सुरक्षितम्।" "What is deposited with the shroff is secure." , Merchant saying

Trust was earned over generations. A shroff house that defaulted didn't just lose customers, it lost its entire network position, often destroying the family permanently. The incentive to maintain trust was existential.

The Hundi as Global Payment System

The hundi network was, functionally, an ancient SWIFT system:

Coverage: Hundis were honored from Southeast Asia to the Mediterranean. Indian merchant networks operated in Egypt, Arabia, Persia, Central Asia, China, and Southeast Asia. Anywhere Indians traded, hundis worked.

Speed: Value could move faster than physical transport. A merchant in Canton could receive credit notification (via faster ships or overland routes) before the goods that generated the credit even arrived.

Efficiency: Transaction costs were minimal, a small commission to the shroff, no transport costs, no insurance on cash, no guards.

Flexibility: Hundis could be denominated in any currency the network handled. A hundi issued in rupees could be paid in Chinese taels or Persian dinars, at prevailing exchange rates.

The British East India Company, when it arrived in India, was astonished by the sophistication. They found a financial system that, in many respects, exceeded European banking.

Global Perspectives: SWIFT and Modern Payment Networks

The hundi system anticipated modern payment infrastructure by two millennia.

SWIFT (Society for Worldwide Interbank Financial Telecommunication), established in 1973, is the global messaging system that enables international bank transfers. When you wire money internationally, SWIFT messages coordinate between banks. The system connects over 11,000 financial institutions in 200+ countries.

SWIFT's architecture mirrors the hundi network:

| Element | Hundi System | SWIFT System |

|---|---|---|

| Network | Shroff correspondent relationships | Member bank relationships |

| Trust | Multi-generational reputation | Regulatory oversight + contracts |

| Message | Physical hundi document | Electronic SWIFT message |

| Settlement | Periodic inter-shroff accounting | Central bank settlement |

| Coverage | Trade route reach | Global membership |

The fundamental insight is identical: value can move through messaging networks faster, cheaper, and safer than through physical transport. Only the technology changed, from paper and trust to electrons and regulation.

The Medici Bank (15th century Florence) developed the bill of exchange that enabled European trade to scale. Lorenzo de' Medici's network of correspondents across Europe worked similarly to shroff networks, local partners who would honor each other's paper because of trust and ongoing relationships.

What distinguishes the Indian system: it was earlier (by over a millennium) and more extensive. The Medici network was European; the shroff network was intercontinental.

The Trust Infrastructure

Hundis worked without courts, without contracts, without formal law. How?

The answer is embedded trust, trust built into social structures rather than legal structures:

Family Networks: Shroff houses were typically family businesses spanning generations. The family's accumulated reputation was its primary asset. A default destroyed not just a business but a lineage.

Community Accountability: Shroffs belonged to communities (Marwaris, Chettiars, Multanis) that enforced internal standards. A shroff who cheated faced community ostracism, no marriages, no partnerships, no future.

Correspondent Dependency: Each shroff depended on correspondents in other cities. Breaking trust with one correspondent risked the entire network. The interconnection created mutual accountability.

Reputation Systems: Information about defaults traveled fast. Merchant networks shared intelligence about unreliable parties. A shroff's reputation was public knowledge throughout the trade world.

This trust infrastructure achieved what modern legal systems struggle to achieve: reliable contract enforcement across jurisdictions. No international court was needed because the costs of defection were prohibitive.

Modern Resonance: UPI and the Digital Hundi

India's Unified Payments Interface (UPI) represents the hundi principle in digital form, perhaps the most significant payment innovation since the hundi itself.

UPI was launched in 2016 by the National Payments Corporation of India (NPCI). Its design echoes shroff networks:

Interoperability: Like hundis honored across shroff networks, UPI payments work across banks. A customer of any UPI-enabled bank can pay any other, regardless of which bank they use.

Instant Settlement: Like darshani hundis payable on sight, UPI settles in real-time. Money moves in seconds, not days.

Trust Infrastructure: UPI works because NPCI provides the trust layer, the modern equivalent of shroff reputation networks. Banks trust each other because NPCI guarantees settlement.

Low Cost: Like hundi commissions, UPI transaction costs are minimal, often zero for consumers. The network's scale makes individual transaction costs negligible.

UPI's scale is extraordinary:

- 12+ billion transactions monthly (2024)

- 50%+ of India's digital payments

- Cross-border expansion to UAE, Singapore, Nepal, and beyond

The pattern is identical: India innovated a payment system that solved real problems (interoperability, speed, cost), scaled it nationally, and is now extending it globally. The shroffs would recognize UPI immediately, it's what they would have built if they had smartphones.

Your Turn

Chandragupta's problem, moving value safely, remains universal. Modern solutions (UPI, SWIFT, cryptocurrency) address the same challenge with different technologies.

The hundi insight persists: value is information, not metal. When you send a UPI payment, no rupee coins move. When you wire money internationally, no dollars cross oceans. Value moves as messages across trust networks, exactly as it did when a shroff wrote a hundi payable 1,500 kilometers away.

Understanding this transforms how you think about money. Physical cash is just one representation of value. Credit systems, digital payments, and cryptocurrencies are all variations on the hundi principle: value as negotiable commitment rather than physical object.

What payment systems do you use? Do you understand the trust infrastructure that makes them work? The shroffs understood that their network was their product. Modern payment providers understand the same: the network is the value.

Money as social construct, value exists through collective agreement, not intrinsic properties of physical objects.

Modern monetary theory (MMT) and chartalism argue that money's value comes from state authority and social acceptance, not gold backing or intrinsic worth. The hundi system demonstrated this practically: community acceptance made paper valuable. Cryptocurrency enthusiasts make similar arguments, Bitcoin has value because people agree it does.

Indian commercial culture treated money as instrumental for millennia. The hundi's existence proves merchants understood money's social nature long before economists theorized it. This cultural comfort with abstract value may explain India's rapid adoption of digital payments, UPI's success reflects an ancient understanding that value is agreement, not metal.

UPI processed 12.02 billion transactions worth Rs 18.53 lakh crore in a single month (October 2024). This astronomical volume moves through digital messages, no physical rupees involved. The hundi insight, scaled to billions.

Trust as infrastructure, the institutional arrangements that make cooperation possible across distances and differences.

Game theory analyzes how repeated interactions create cooperation incentives. The 'shadow of the future', knowing you'll interact again, discourages cheating. Shroff networks institutionalized this: community membership meant indefinitely repeated games where defection was suicidal. Robert Putnam's social capital research shows similar patterns: trust-rich communities achieve economic outcomes that low-trust communities cannot.

Verses

निक्षेपो यः श्रेष्ठिषु न्यस्तः स सुरक्षितः।

nikṣepo yaḥ śreṣṭhiṣu nyastaḥ sa surakṣitaḥ |

A deposit placed with shroffs is secure.

Financial intermediation requires trust. Shroffs earned trust through reputation, community accountability, and generations of reliable service. Modern banks achieve similar trust through regulation and deposit insurance. The function is identical; the mechanism differs.

Arthashastra, 2.5.13 (R.P. Kangle)

हुण्डिकायां यो व्याजः तत्प्रमाणं विनिश्चितम्।

huṇḍikāyāṃ yo vyājaḥ tatpramāṇaṃ viniścitam |

The interest or discount on a hundi is fixed at a determined rate.

Financial literacy was widespread. Merchants could calculate complex transactions because mathematical education included commercial applications. This human capital, financial numeracy, was as important as the hundi instrument itself.

Lilavati, Commercial Arithmetic Section (Kim Plofker)

वृद्धिः साग्रमशीतिः स्यान्मासस्य विंशतिः शतम्।

vṛddhiḥ sāgramaśītiḥ syānmāsasya viṃśatiḥ śatam |

Interest should not exceed eighty percent annually; twenty percent per month is the maximum.

Interest rate regulation balances creditor protection with debtor protection. Ancient texts recognized that unregulated lending could become exploitative while acknowledging that lenders needed compensation for risk. The debate continues in modern usury laws and interest rate caps.

Manusmriti, 8.151 (Patrick Olivelle)

Key figures

The Shroff Networks (Marwari, Chettiar, Multani)

Community-based banking networks that created the infrastructure for hundi systems, interconnected families and firms that trusted each other across vast distances. · c. 300 BCE - present

Nandan Nilekani

Co-founder of Infosys and architect of India's digital public infrastructure, Aadhaar (digital identity), UPI (digital payments), and related systems. · Contemporary (b. 1955)

SWIFT (Society for Worldwide Interbank Financial Telecommunication)

The global messaging system enabling international bank transfers, the modern infrastructure for cross-border payments. · 1973 - present

Case studies

UPI: The Digital Hundi Conquers the World

In 2016, India faced a payment problem eerily similar to ancient merchants': how to move value efficiently across a vast, fragmented system. India had dozens of banks, multiple payment systems (NEFT, RTGS, IMPS), and no interoperability. Sending money from one bank to another required knowing account numbers, IFSC codes, and waiting hours or days for settlement. Digital payments were growing but remained complex and expensive. The **Unified Payments Interface (UPI)**, developed by the National Payments Corporation of India (NPCI), was designed to solve this, and its design explicitly drew on India's commercial heritage. UPI's architecture mirrors hundi networks: **Virtual Payment Address (VPA)**: Like a hundi's named payee, UPI uses simple addresses (yourname@bankupi) rather than complex account numbers. Anyone can send to anyone without knowing bank details. **Instant Settlement**: Like darshani hundis payable on sight, UPI settles in real-time. Money moves in seconds, not days. **Interoperability**: Like shroff correspondent networks, UPI connects all member banks. A payment from any bank reaches any other bank, the modern equivalent of a hundi honored across the shroff network. **Low Cost**: Like hundi commissions, UPI costs are minimal, often zero for consumers. The network's scale makes per-transaction costs negligible.

UPI embodies hundi principles digitized: **Vishwas (Trust)**: UPI works because NPCI provides trust infrastructure. Banks trust each other because NPCI guarantees settlement. This is the modern equivalent of shroff community trust, institutionalized and regulated rather than reputation-based. **Sarva-Sulabha (Universal Access)**: UPI was designed for inclusion, feature phones, regional languages, small merchants. The shroff networks served everyone who could pay their commission; UPI serves everyone with a phone. **Practical Innovation**: UPI solved real problems (interoperability, speed, cost) with practical design. Like hundis that evolved multiple types (darshani, muddati, jokhmi) for different needs, UPI evolved features (autopay, mandate, international) for different use cases. The dharmic insight: financial infrastructure is public good. Like roads and water, payment systems enable everything else. India's willingness to build public digital infrastructure, rather than leaving it to private fragmentation, reflects ancient understanding that commerce needs shared foundations.

UPI's growth has been extraordinary: **Volume**: From 0 transactions (April 2016) to 12+ billion monthly transactions (2024), the world's largest real-time payment system. **Value**: Over Rs 18 lakh crore ($216 billion) monthly transaction value. **Adoption**: 300+ million users, 50+ million merchants, 400+ banks. **Global Expansion**: UPI now works in UAE, Singapore, Nepal, Bhutan, France, and expanding. Indian travelers can pay abroad using UPI; eventually, the world may use UPI-like systems. The geopolitical significance: India has built payment infrastructure that rivals, and in some ways exceeds, anything in the developed world. UPI's success demonstrates that ancient commercial wisdom, properly adapted, creates global advantage. The shroffs would recognize UPI immediately. It's what they built, digitized and scaled. Value moving through trusted networks, instantly, across any distance. The hundi principle, reborn.

Financial innovation builds on cultural foundations. UPI succeeded partly because Indians are culturally comfortable with abstract value transfer, a comfort that the hundi system created over millennia. Understanding your cultural heritage can reveal competitive advantages invisible to outside observers.

UPI's global expansion to Singapore, UAE, France, and Sri Lanka follows the pattern of successful payment infrastructure exports. China's Alipay and WeChat Pay expanded similarly. The competitive advantage goes to systems that are interoperable, low-cost, and built for mass adoption from day one.

UPI processed more real-time transactions in 2023 than all other real-time payment systems combined, including the US, EU, and China. India went from payment laggard to payment leader in under a decade by building on ancient commercial insights.

Hawala: The Hundi That Never Died

In modern Dubai, a Pakistani construction worker wants to send money to his family in Karachi. He could use a bank, but banks are slow, expensive, and his family may not have accounts. Instead, he visits a **hawaladar**. The hawaladar takes his dirhams, makes a phone call to his correspondent in Karachi, and within hours, his family receives rupees. No money physically moved. No bank was involved. The transaction was recorded only in the hawaladars' private ledgers. This is **hawala**, the direct descendant of the ancient hundi system, still operating globally. Hawala works identically to hundis: **Correspondent Networks**: Hawaladars maintain relationships with correspondents in other locations. Trust is based on community ties (often ethnic: Pakistani, Somali, Indian) and repeated business. **Messaging**: Value transfers through communication (phone, WhatsApp, encrypted apps) rather than physical movement. The hawaladar in Dubai informs his correspondent in Karachi; the correspondent pays out locally. **Settlement**: Hawaladars settle periodically, not per transaction. Flows roughly balance (migration goes one way, trade the other), so net settlement needs are minimal. **Cost**: Hawala fees are typically 1-3%, lower than bank wire transfer costs, especially for small amounts.

Hawala demonstrates the persistence of hundi principles: **Trust over Regulation**: Hawala operates largely outside formal regulation, yet fraud is rare. Community trust and reputation enforcement work. A hawaladar who cheats loses everything, exactly as a shroff would have. **Efficiency through Simplicity**: Hawala eliminates intermediaries that formal systems require. Value moves through two contacts (sending hawaladar, receiving hawaladar) rather than through banks, correspondent banks, and clearing systems. **Service to the Underserved**: Hawala serves migrants, refugees, and others poorly served by formal banking. This echoes the shroff tradition of serving whoever could pay, not just the wealthy or documented. The dharmic tension: hawala is also used for money laundering, tax evasion, and illicit finance. The same features that make it efficient for migrants make it efficient for criminals. This is the shadow side of trust systems: they serve whoever can access them.

Hawala's scale is difficult to measure precisely (it's largely informal), but estimates suggest: **$200-500 billion annually** in global hawala flows, more than many countries' GDPs. **Critical role in remittances**: Many migration corridors (South Asia to Gulf, Somalia diaspora, etc.) depend heavily on hawala. **Regulatory ambivalence**: Most countries technically prohibit unlicensed hawala, but enforcement is uneven. The systems persist because they serve real needs that formal banking doesn't. Hawala represents the hundi's survival into modernity, adapted but recognizable. The trust networks that enabled ancient trade now enable global migration remittances. The technology changed (phones instead of paper); the principle didn't. For India, hawala presents both heritage and challenge. The system reflects Indian commercial genius, but its informal nature creates regulatory and security concerns. Modern UPI offers a regulated alternative that captures hundi efficiency while addressing hawala's vulnerabilities.

Financial innovations that solve real problems persist across millennia. Hawala survives despite regulation because it meets needs formal systems don't. Understanding why people use informal systems reveals opportunities for formal innovation, which is exactly what UPI represents.

Hawala's persistence despite decades of regulation reveals a core fintech insight: informal financial systems survive because they solve real problems that formal systems ignore. M-Pesa in Kenya succeeded by addressing the same gap. Effective financial innovation starts from understanding why people use informal channels.

The World Bank estimates that hawala handles 50%+ of remittances to some countries (Afghanistan, Somalia). For India, formal channels dominate, but hawala remains significant for certain corridors and purposes. The hundi's descendants remain economically important.

Historical context

c. 300 BCE - present (continuous evolution)

The hundi system enabled India's ancient trade dominance. Merchants could operate across continents because shroff networks provided payment infrastructure that physical cash could never match. The British found the system so sophisticated that they initially relied on shroff networks before establishing their own banking. Post-independence, formal banking marginalized shroffs, but informal systems (hawala) persisted. UPI represents recovery of indigenous payment principles in modern form.

The Italian bill of exchange (13th-15th centuries) developed similar functions in European trade, but later and with more limited geographic reach. The Medici banking network was revolutionary for Europe but comparable to what shroffs had achieved centuries earlier across wider distances. Modern SWIFT (1973) finally created a global messaging system for payments, essentially industrializing what hundi networks had done for millennia.

Roman historian Pliny complained that Rome's gold was draining to India, evidence of the trade surplus that required sophisticated payment systems. Roman gold found in India (Muziris excavations) confirms the scale of trade that hundi systems facilitated.

UPI's global success demonstrates that ancient Indian financial innovation remains competitive. Understanding hundi principles illuminates why UPI works, why India adopted digital payments so rapidly, and why payment infrastructure is strategic national capability. The commercial wisdom encoded in hundis is now powering India's digital economy.

Living traditions

- UPI instant payments

- Hawala/informal value transfer

- Trade credit among jewelers

- Zaveri Bazaar: Historic gold trading center where traditional shroff functions continue. Gold dealers also provide money-changing, trade credit, and financial services, the integrated shroff model in modern form.

- NPCI Innovation Hub: The National Payments Corporation of India develops and operates UPI. Tours and exhibitions explain how India's digital payment infrastructure works.

- Meenakshi Temple: Ancient trade hub where merchant financiers operated. Temple treasury functioned as early banking institution, accepting deposits and financing trade expeditions along southern routes.

- Tirupati Balaji Temple: World's richest temple with sophisticated financial operations. Manages billions in assets using systems descended from shreni banking, including gold deposits and investment management.

Reflection

- The hundi separated value from physical form, a piece of cloth could be worth thousands of gold coins. Modern digital payments complete this separation. How does your understanding of money change when you recognize it as agreement rather than object?

- Shroff networks worked because trust was more valuable than any single transaction. In your professional life, what is your 'correspondent network', the people whose trust you've earned and who would honor your commitments? How deliberately are you building it?