India Stack: डिजिटल पब्लिक इंफ्रास्ट्रक्चर

1.4 अरब के लिए डिजिटल परत का निर्माण

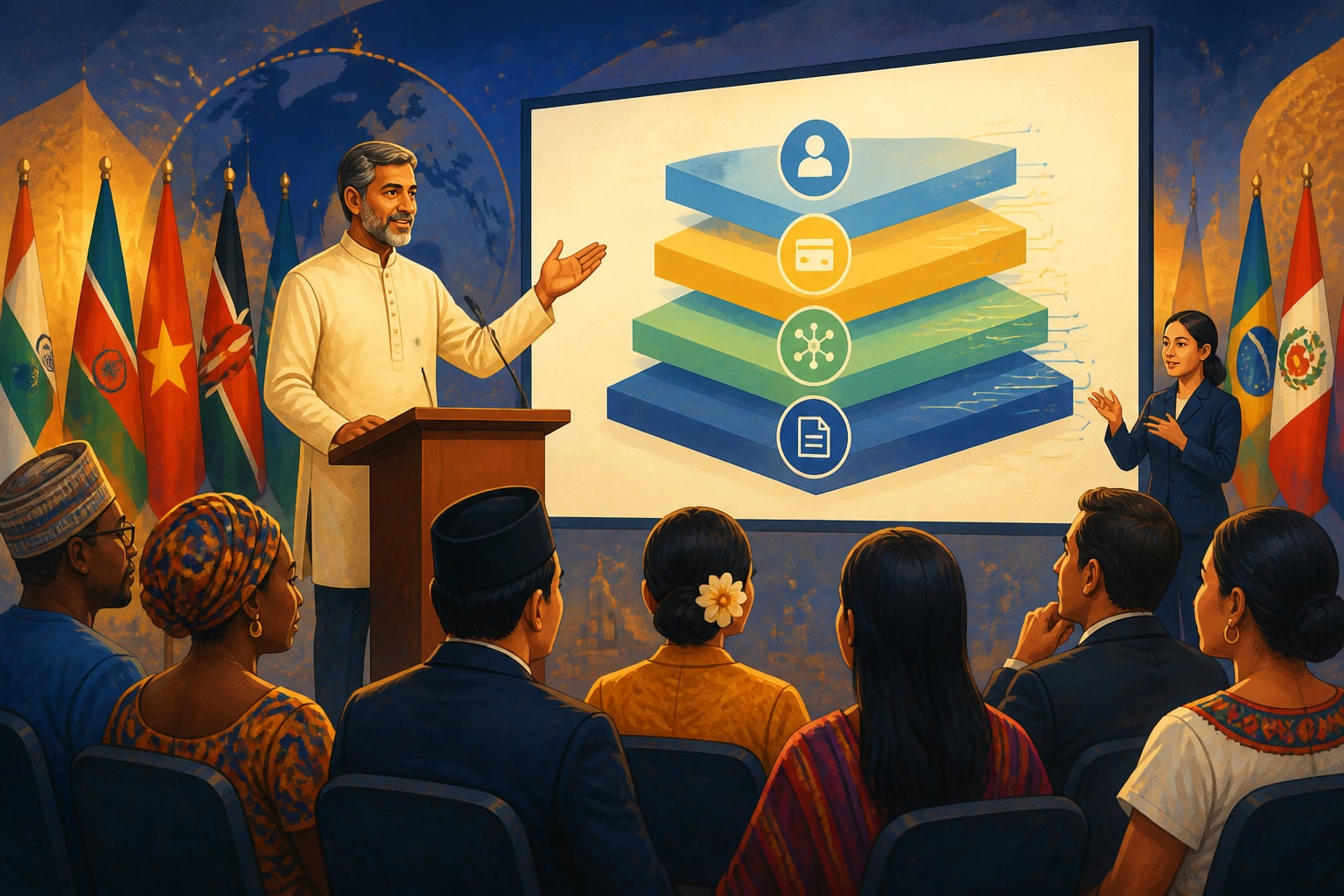

यूपीआई सिर्फ एक बड़ी चीज़ की एक परत है: India Stack, एक व्यापक डिजिटल इंफ्रास्ट्रक्चर जो पहचान, पेमेंट्स, डेटा शेयरिंग, और दस्तावेज़ वेरिफिकेशन को एक साथ लाता है। यह पाठ बाहर निकलकर India के Digital Public Infrastructure (DPI) की पूरी आर्किटेक्चर को देखता है, कैसे कई परतें एक साथ काम करती हैं 10-मिनट के लोन जैसी सेवाएं संभव बनाने के लिए, और क्यों भारत अब यह मॉडल दुनियाभर में एक्सपोर्ट कर रहा है।

10 मिनट का लोन

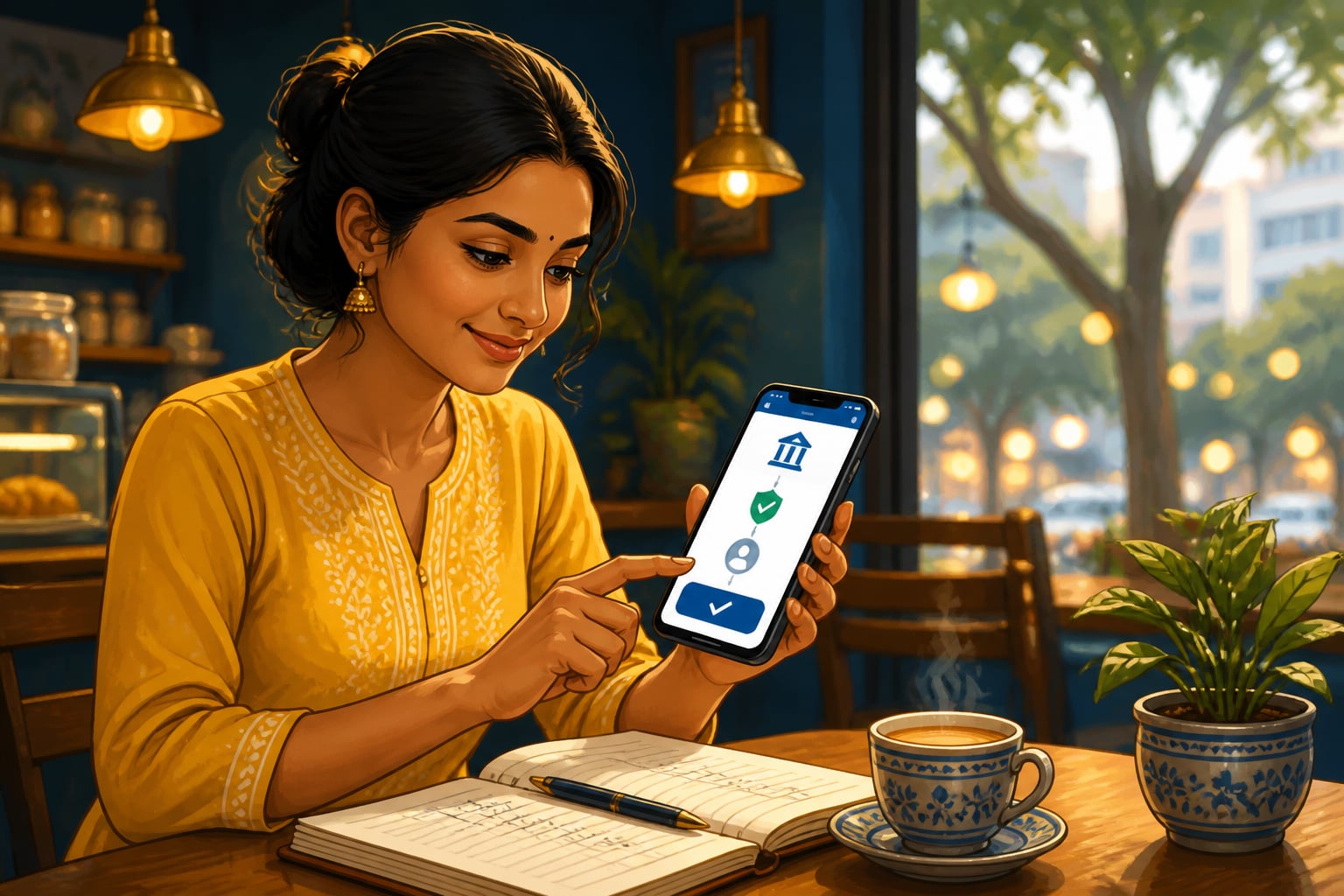

Rajesh Sharma runs a small electronics repair shop in Jaipur. In November 2023, he needed ₹2 lakh to stock inventory for Diwali season. In the old world, this meant weeks of paperwork: bank statements, ITR copies, property documents as collateral, multiple branch visits, and probably rejection because small shopkeepers don't have the documentation banks traditionally require.

Instead, Rajesh opened a lending app on his phone. He authenticated with his Aadhaar number and fingerprint. The app asked for consent to access his financial data, specifically, his GST returns and bank statements from the past two years. He tapped 'Allow.'

Behind the scenes, something remarkable happened. The app connected to the Account Aggregator network, which securely fetched his financial data from multiple sources, his bank, the GST portal, his credit history, all with his explicit consent. An AI system analyzed two years of cash flows, his consistent GST filings, his UPI transaction history as a merchant.

Within 10 minutes, Rajesh received an offer: ₹2 lakh at 14% annual interest, no collateral required. He accepted. The money arrived in his Jan Dhan account via UPI before he finished his chai.

What enabled this wasn't just one technology, it was India Stack: multiple layers of digital infrastructure working together. Aadhaar verified his identity. Account Aggregator shared his financial data. UPI moved the money. Each layer built on the others, creating capabilities that none could achieve alone.

What Is India Stack?

India Stack isn't a single system, it's a collection of interoperable digital public goods that together create a digital layer for the Indian economy. Think of it as the digital infrastructure on which private innovation builds, like how roads enable transportation businesses.

The stack has four primary layers:

Layer 1: Identity (Aadhaar)

What it does: Provides a unique, biometrically-verified digital identity to every resident Scale: 1.4 billion enrollees, 99% of adult population Key capability: eKYC, verify someone's identity remotely in seconds

Layer 2: Payments (UPI)

What it does: Enables instant, interoperable digital payments between any two parties Scale: 16+ billion transactions monthly, ₹300+ lakh crore annually Key capability: Real-time money movement at zero cost

Layer 3: Data (Account Aggregator)

What it does: Allows individuals to share their financial data with institutions through secure, consent-based protocols Scale: Launched 2021, growing rapidly with 10+ million consent requests Key capability: Financial history becomes portable, controlled by the individual

Layer 4: Documents (DigiLocker)

What it does: Stores verified government documents digitally, shareable with a click Scale: 200+ million users, 6+ billion documents Key capability: Paperless verification for everything from driving licenses to degrees

स्तर-स्तरे व्यवस्था, मूले राज्य-मञ्चः

Stara-stare vyavasthā, mūle rājya-mañcaḥ

"Layer upon layer the system builds; at the foundation, the state's platform."

This architectural principle, public infrastructure enabling private innovation, distinguishes India Stack from both the Chinese model (state-controlled super-apps) and the American model (private platforms extracting from users).

The Kautilyan Vision: State as Enabler

India Stack embodies a principle from the Arthashastra: the state should create conditions for commerce, not conduct commerce itself.

राजा यानपथान् कुर्यात्, यानानि जनाः स्वयम्

Rājā yānapathān kuryāt, yānāni janāḥ svayam

"Let the king build the roads; the people will bring their own vehicles."

Kautilya advocated for state investment in infrastructure, roads, waterways, markets, that enabled private trade. He didn't recommend the king run shops; he recommended the king create conditions where shops could thrive.

India Stack follows this philosophy. The government built Aadhaar, the Account Aggregator framework, DigiLocker, but private companies build the apps, the lending platforms, the services that use this infrastructure. PhonePe didn't build payment rails; NPCI did. PhonePe built an excellent experience on top of shared rails.

This is Digital Public Infrastructure (DPI): government builds the platform; markets build on the platform.

Global Perspectives: Why the World Is Watching

India's DPI approach is now being studied and replicated worldwide. During India's G20 presidency in 2023, DPI became a central theme, PM Modi explicitly positioned India Stack as a model for the Global South.

Countries adopting India's model:

- Singapore: UPI-PayNow linkage allows instant cross-border payments between India and Singapore

- UAE: UPI now works in the Emirates; broader DPI discussions ongoing

- African nations: Several countries exploring India Stack-like infrastructure with Indian technical assistance

- France: Studying India's digital payments for potential European implementation

Pramod Varma, the chief architect of Aadhaar and key designer of India Stack, now works with governments worldwide through the Digital Public Goods Alliance. His message: "You don't have to build from scratch. India's code is open-source. Our mistakes and learnings are documented. Build on what we've done."

The contrast with other models is stark:

| Approach | Examples | Philosophy | Outcome |

|---|---|---|---|

| Indian DPI | India Stack | State builds infrastructure; private sector builds services | Open, interoperable, inclusive |

| Chinese Super-Apps | Alipay, WeChat | Private platforms become gatekeepers; state controls platforms | Closed ecosystems, but massive scale |

| American Platforms | Google, Apple, Meta | Private platforms extract value; state is passive | Innovation, but exclusion and extraction |

The key insight: India created a third way, neither state-controlled commerce nor unchecked platform capitalism, but public infrastructure enabling private innovation.

Account Aggregator: The New Layer

The newest layer of India Stack, and perhaps the most transformative, is the Account Aggregator (AA) framework, launched in September 2021.

The problem AA solves: information asymmetry in lending. Banks don't lend to small businesses because they can't verify income. Small businesses can't prove income because their data is scattered across multiple sources (bank accounts, GST filings, invoices). The result: credit doesn't flow to those who need it most.

AA creates a consent-based data sharing infrastructure:

- Financial Information Providers (FIPs): Banks, GSTN, insurance companies, hold your data

- Financial Information Users (FIUs): Lenders, wealth managers, need your data

- Account Aggregators: Licensed intermediaries that move data from FIPs to FIUs, based on your explicit consent

Critically, AAs cannot see or store your data. They're pipes, not repositories. Data flows encrypted end-to-end; the AA just facilitates the connection. This is privacy by design.

स्व-दत्तानुमतिः मूलम्, न परस्य विवेचनम्

Sva-dattānumatiḥ mūlam, na parasya vivecanam

"One's own given consent is the foundation, not another's discretion."

This principle, that individuals control their own data, is revolutionary. In most systems, institutions hold your data and share it at their discretion. In AA, you decide what to share, with whom, for how long.

Modern Resonance: Credit for the Uncreditable

The immediate impact of Account Aggregator is on lending. India has a massive credit gap: the difference between demand for credit and available supply. For MSMEs (Micro, Small, and Medium Enterprises), this gap is estimated at ₹25+ lakh crore.

Why? Because traditional lending requires collateral, audited financials, and credit history, things small businesses lack. A vegetable vendor, a neighborhood electrician, a small manufacturer, they may have steady cash flows but no assets to pledge.

AA changes this. Now, a lender can see:

- GST filings: Proof of regular business activity and revenue

- Bank statements: Cash flow patterns across accounts

- Other accounts: Full financial picture, not just what the applicant selects

With this data, AI models can assess creditworthiness without collateral. The lender knows that Rajesh the electronics repairer has filed GST for 24 consecutive months, receives consistent UPI payments from customers, and maintains positive bank balances. That's enough to lend ₹2 lakh.

Early results (as of 2024):

- 10+ million consent requests processed through AA network

- Multiple banks and NBFCs offering 'digital flow-based lending'

- Average loan approval time dropping from weeks to minutes

- Credit reaching segments that were previously 'unbankable'

This is India Stack's power: not any single layer, but the combination of layers creating capabilities impossible with any alone.

The Stack Philosophy: Layers Building on Layers

India Stack's design reflects a deeper philosophy: complex systems are built in layers, with each layer creating the foundation for the next.

Consider how Rajesh's 10-minute loan required every layer:

- Aadhaar verified Rajesh is who he claims

- eKYC allowed the lender to onboard him remotely

- Account Aggregator fetched his financial data with consent

- UPI delivered the loan to his account

- Jan Dhan ensured he had a bank account to receive it

Remove any layer, and the loan doesn't happen. The power is in the integration.

This mirrors ancient Indian systems of knowledge that emphasized interdependence:

एकः शक्नोति यत् कर्तुं, बहवः कुर्वन्ति तत् शतगुणम्

Ekaḥ śaknoti yat kartuṃ, bahavaḥ kurvanti tat śataguṇam

"What one can do, many together do a hundredfold."

The stack isn't a single hero technology, it's coordinated infrastructure where each piece amplifies the others.

Your Turn: Living in the Stack

You're already embedded in India Stack, probably without realizing it:

- Aadhaar-based eKYC verified your mobile connection, bank account, mutual fund investments

- UPI handles your daily payments

- DigiLocker may hold your driving license, vehicle registration, vaccine certificates

- Account Aggregator might already have processed requests for your data (check your bank's consent dashboard)

This is infrastructure so successful it becomes invisible, like electricity or roads. You don't think about UPI as 'India Stack Layer 2'; you just pay.

But here's the deeper question: What new capabilities does this infrastructure enable that we haven't imagined yet?

When roads were built, no one anticipated the trucking industry, roadside restaurants, or highway tourism. When the internet was built, no one anticipated social media or streaming video. Infrastructure creates possibilities that exceed the imagination of its builders.

India Stack is young, Aadhaar is 15 years old, UPI is 8, Account Aggregator is 3. What will be built on this foundation in the next decade? Small business credit is just the beginning. Health data sharing, education credentials, land records, supply chain finance, all could be transformed by consent-based, interoperable digital infrastructure.

In our next lesson, we'll meet Nandan Nilekani, the architect who envisioned and led the creation of this stack. You'll understand the philosophy behind the design and the battles fought to build it.

Economists debate the state's role in markets. Libertarians argue for minimal state involvement; socialists argue for state control. Kautilya, and India Stack, propose a third way: the state as platform builder. The US government built the internet (ARPANET); private companies built Google and Facebook on top. India Stack makes this pattern explicit and intentional.

India's tradition of seeing the state as facilitator (rather than either absent or controlling) made DPI design intuitive. The philosophical groundwork existed; India Stack operationalized it for the digital age. Countries without this tradition struggle to find the right balance between state and market in digital infrastructure.

India Stack required approximately ₹10,000-15,000 crore in public investment (across Aadhaar, NPCI, etc.) over 15 years. The private sector has built services worth ₹5+ lakh crore in market capitalization on this foundation. That's a 30x+ return on public investment.

The European GDPR gives individuals data rights, but enforcement is difficult. American law leaves data largely in corporate hands. India's AA creates a technical implementation of consent: data literally cannot move without user authorization. This is consent by architecture, not just by law.

India's AA framework is the world's most advanced implementation of consent-based data sharing at scale. It's not just a legal right but a technical reality: Financial Information Providers cannot share data without a user-authorized request through an Account Aggregator. The system enforces the principle.

In traditional lending, the bank holds all power: they have your data and decide whether to lend. With AA, you hold power: you decide which data to share, with whom, for how long. This shift, from institutional discretion to individual sovereignty, is revolutionary.

Key terms

- Bharat Stack (India Stack)

- आपस में जुड़े डिजिटल पब्लिक गुड्स का एक संग्रह, आधार, यूपीआई, Account Aggregator, और DigiLocker को शामिल करते हुए, जो एक साथ भारतीय अर्थव्यवस्था की डिजिटल इंफ्रास्ट्रक्चर परत बनाते हैं।

- Khata-Samaharta (Account Aggregator)

- एक सहमति-आधारित फ्रेमवर्क जो लोगों को अपना फाइनेंशियल डेटा कई संस्थाओं (बैंक्स, जीएसटीएन, insurance) से सेवा प्रदाताओं के साथ share करने देता है secure, regulated intermediaries के ज़रिए।

- DigiLocker

- एक सरकारी प्लेटफॉर्म जो दस्तावेज़ों की verified digital copies store करता है, driving licenses, educational certificates, vehicle registration, जिन्हें एक क्लिक से share किया जा सकता है, physical paperwork की ज़रूरत खत्म करते हुए।

- Sahamati-Adharit Sahajakaran

- Consent-based sharing, एक data governance सिद्धांत जहां जानकारी सिर्फ data owner की explicit, informed सहमति के साथ चलती है, जो किसी भी समय सहमति वापस ले सकता है।

Key figures

कौटिल्य की राज्य-ढांचे की दृष्टि

State की भूमिका को platform builder के रूप में conceptualized किया, service provider नहीं। Mauryan Empire ने Grand Trunk Road नहीं बनाया transportation company operate करने के लिए, बल्कि सभी traders को efficiently goods move करने के लिए enable करने के लिए। यह philosophy, state infrastructure बनाता है, markets infrastructure पर build करते हैं, Digital Public Infrastructure का मूल है।

प्रमोद वर्मा

India Stack को काम करने वाली technical architecture design की, the APIs, protocols, और privacy frameworks जो different layers को securely interoperate करने देती हैं। 'design for a billion' सोच को championed किया: ऐसे solutions जो India के scale और diversity के लिए काम करें, सिर्फ urban elites के लिए नहीं।

मरियाना मज़ुकातो

Government investment in digital infrastructure क्यों important है, यह समझने के लिए theoretical framework provide किया। इस common view के against कि innovation सिर्फ private sector से आता है, Mazzucato ने दिखाया कि iPhone, internet, और GPS सभी decades की government investment पर depend करते थे। India Stack उनकी thesis को prove करने वाला एक case study है।

Case studies

Account Aggregator: उन लोगों के लिए क्रेडिट जिन्हें असंभव माना जाता था

Account Aggregator से पहले, भारत में small business lending बिल्कुल टूटा हुआ था। बैंक के पास पैसे उधार देने के लिए थे; small businesses को क्रेडिट चाहिए था; लेकिन वे connect नहीं कर सकते थे। समस्या information की थी। Permanent lending को चाहिए: - **गिरवी**: अगर लोन default हो तो अगर कुछ asset बेचे - **Audited financials**: income और expenses का proof - **क्रेडिट हिस्ट्री**: repayment का track record ज़्यादातर small businesses, kirana store, auto repair shop, neighborhood tailor, के पास इनमें से कोई नहीं है। वे cash में operate करते हैं; उनके पास chartered accountant-prepared statements नहीं हैं; उन्हें कभी formal credit नहीं मिला है। लेकिन उनके पास **financial footprints** हैं: - **जीएसटी फाइलिंग्स**: अगर registered हैं, तो वे monthly returns file करते हैं जो turnover दिखाते हैं - **बैंक स्टेटमेंट्स**: नकद प्रवाह visible है, भले ही audited न हो - **यूपीआई लेनदेन**: merchants के रूप में, उनकी sales recorded हैं समस्या: यह डेटा silos में बैठा था। GST portal बैंक्स से talk नहीं कर सकता था; बैंक्स दूसरे बैंक्स की statements access नहीं कर सकते थे; lenders पूरी तस्वीर नहीं देख सकते थे। Account Aggregator ने यह solve किया **consent-based data pipeline** बनाकर: 1. Borrower डेटा share करने के लिए सहमति देता है 2. AA कई sources (GST, banks, आदि) से डेटा खींचता है 3. डेटा encrypted होकर lender तक बहता है 4. Lender का AI creditworthiness assess करता है 5. सप्ताहों नहीं, मिनटों में loan का फैसला पहला AA-enabled लोन सितंबर 2021 में disbursed किया गया था। 2024 तक, यह ecosystem millions of consent requests को process कर रहा था।

Account Aggregator एक fundamental injustice को address करता है: लोगों को जिनके पास repay करने की genuinely क्षमता थी, credit deny किया गया क्योंकि वे इसे traditional तरीकों से prove नहीं कर सकते थे। यह है **epistemic injustice**, disadvantaged होना क्योंकि system आपकी reality को 'see' नहीं कर सकता। Dharmic सोच value और proof के कई forms को recognize करती है। एक vegetable vendor की consistent GST filings एक corporate के audited financials जितनी ही valid indicator हैं creditworthiness की, system सिर्फ पहले उन्हें read नहीं कर सकता था। AA **न्याय** (justice) create करता है जो हमेशा वहां था उसे visible बनाकर। Consent फ्रेमवर्क dharmic respect को autonomy के लिए embody भी करता है। institutions decide करने की जगह कि आपके बारे में क्या share करें, आप decide करते हो। यह है **स्वधर्म** data पर लागू होना: आपकी जानकारी, आपकी choice।

**शुरुआती नतीजे (2024 तक)**: - AA नेटवर्क के ज़रिए 10+ मिलियन consent requests processed - कई lenders 'digital flow-based lending' products offer कर रहे हैं - Average loan approval time: सप्ताहों की जगह मिनट - पहले 'unbankable' माने जाने वाले segments तक credit पहुंच रहा है - Digitally-active businesses के लिए MSME credit gap बंद होने लगा है **Qualitative प्रभाव**: - राजेश इलेक्ट्रॉनिक्स repairer दिवाली के लिए स्टॉक कर सकता है - लक्ष्मी vegetable vendor अपनी stall expand कर सकती है - Ideas वाले entrepreneurs लेकिन बिना assets के capital access कर सकते हैं - Formal financial system finally informal economy तक पहुंच गया है

Information infrastructure market failures को solve कर सकता है जिन्हें न regulation और न ही competition fix कर सकता है। बैंक्स छोटे businesses को लोन refuse नहीं कर रहे थे malice से; वे genuinely creditworthiness assess नहीं कर सकते थे। AA ने missing infrastructure provide किया, एक ऐसा market enable करता है जो दोनों sides चाहते थे लेकिन अकेले create नहीं कर सकते थे।

Open banking regulations in the UK, EU, and Australia are all attempting what India's Account Aggregator framework achieves: giving users control over their financial data to unlock better credit access. India's consent-based architecture is being studied as a model that balances innovation with privacy.

भारत का MSME credit gap 25+ लाख करोड़ रुपये पर estimated है। अगर AA-enabled lending इस gap का सिर्फ 10% भी close करे, तो वह 2.5 लाख करोड़ रुपये है जो small businesses को flow करेगा जो पहले credit access नहीं कर सकते थे। Economic multiplier effects बहुत बड़े हैं।

India Stack ग्लोबल जाता है: DPI एक Export के रूप में

2023 में भारत की G20 की अध्यक्षता के दौरान, एक remarkable shift हुआ: भारत, जो परंपरागत रूप से technology importer था, खुद को technology exporter के रूप में स्थापित किया। यह export hardware या software products नहीं था; यह **Digital Public Infrastructure** एक model के रूप में था। Pitch सरल था: भारत ने developing countries जो समस्याएं face करते हैं, identity, payments, data, उन्हें solve किया था open, interoperable, low-cost systems using करके। दूसरे देश यह scratch से build करने की जगह replicate कर सकते थे या expensive foreign systems पर निर्भर रह सकते थे। **Key moments**: - **UPI-PayNow linkage (2023)**: भारत और Singapore के बीच direct real-time payment corridor, पहला international UPI link - **UPI in UAE (2023)**: भारतीय यूपीआई apps अब UAE के merchants पर काम करते हैं; broader DPI discussions चल रहे हैं - **African Union engagement**: कई African countries India Stack जैसे infrastructure को explore कर रहे हैं, भारतीय technical assistance के साथ - **G20 DPI declaration**: Leaders ने interoperable, open, inclusive DPI के principles को endorse किया **क्या export किया जा रहा है**: 1. **Architecture और design principles**: Layered, interoperable DPI कैसे build करें 2. **Open-source code**: Core Aadhaar और यूपीआई code adaptation के लिए उपलब्ध है 3. **Technical assistance**: भारतीय experts दूसरे देशों की implementations में advise कर रहे हैं 4. **Lessons learned**: क्या काम किया, क्या fail हुआ, भारत की mistakes कैसे avoid करें

भारत का DPI export एक dharmic सिद्धांत को reflect करता है: ज्ञान को share किया जाना चाहिए, hoard नहीं किया जाना चाहिए। **विद्या-दान** (ज्ञान का उपहार) की ancient परंपरा मानती थी कि ज्ञान को share करने से उसकी value गुणा हो जाती है; इसे secret रखने से वह कम हो जाता है। India Stack को open-source करके और actively दूसरे देशों को इसे replicate करने में मदद देकर, भारत modern विद्या-दान को practice कर रहा है। यह सिर्फ altruism नहीं है, यह influence बनाता है, relationships build करता है, और भारत को technology leader के रूप में position करता है। लेकिन share करने की willingness rather than extract करना (जैसे Western tech companies करते हैं) dharmic सोच को reflect करता है ज्ञान को common goods के रूप में। यह **वसुधैव कुटुम्बकम्** (दुनिया एक परिवार है) को practice में demonstrate भी करता है। Identity, financial inclusion, और digital access की समस्याएं global हैं; भारत के solutions globally help कर सकते हैं। G20 की अध्यक्षता ने इस संदेश को amplify किया: DPI एक competitive advantage नहीं है जिसे hoard किया जाए बल्कि एक public good है जिसे share किया जाए।

**Concrete नतीजे**: - यूपीआई-PayNow live है, India-Singapore payments को instant enable करता है - UAE, Bhutan, Nepal, Singapore में यूपीआई acceptance बढ़ रहा है - कई African nations DPI discussions के various stages में हैं - G20 DPI principles को world की largest economies ने endorse किया **Strategic नतीजे**: - भारत को DPI pioneer और thought leader के रूप में recognize किया गया है - 'India Stack' DPI approach के लिए global shorthand बन गया है - Developing countries के पास Chinese/American tech dependency का alternative है - भारत technical leadership के ज़रिए soft power build कर रहा है **Ongoing चुनौतियां**: - हर देश को अपने local context के लिए customization की ज़रूरत है - Privacy और data sovereignty की चिंताएं jurisdiction के हिसाब से अलग हैं - Implementation की capacity बहुत अलग है - Exported systems की long-term sustainability पर ध्यान देने की ज़रूरत है

Technology leadership सिर्फ products build करने के बारे में नहीं है, यह ऐसे models build करने के बारे में है जिन्हें दूसरे replicate कर सकें। भारत की DPI को open-source और share करने की willingness एक ऐसा influence बनाती है जो proprietary systems नहीं बना सकते। यह soft power का एक नया form है: infrastructure diplomacy।

The concept of Digital Public Infrastructure (DPI) as a national export is now a recognized category in international development. Countries that build replicable, open-source digital systems gain soft power that outlasts any trade agreement or military alliance.

World Bank का estimate है कि DPI developing countries के लिए GDP का 3-13% contribute कर सकता है। अगर सिर्फ 10 देश भी अगले दशक में India Stack-style DPI को successfully implement करें, तो भारत global development में traditional aid के दशकों से ज़्यादा contribute कर चुका होगा।

Historical context

4थी शताब्दी ईसा पूर्व से 2024

भारत की state-built infrastructure की परंपरा जो private commerce को enable करती है, हज़ारों साल पुरानी है। Mauryan road network, Mughal sarais (rest houses), British railways, हर era में state ने infrastructure में investment किया जो trade को enable करता था। India Stack इस परंपरा को digital form में continue करता है, ancient principles को modern technology पर apply करते हुए।

ज़्यादातर देश या तो American model को follow करते हैं (private platforms, minimal state role) या Chinese model को (state-controlled digital systems)। भारत का DPI approach, state open infrastructure build करता है, private sector इसके ऊपर build करता है, एक genuine तीसरा रास्ता है। यह model अब globally study और replicate किया जा रहा है, भारत को digital infrastructure pioneer के रूप में position करते हुए।

India Stack की layers collectively 1 billion से ज़्यादा भारतीयों को छूती हैं: 1.4 billion आधार नंबर, 530 मिलियन Jan Dhan accounts, 16+ billion monthly यूपीआई transactions। कोई दूसरा देश इतने बड़े स्तर पर digital infrastructure नहीं build करता है।

India Stack को integrated infrastructure के रूप में समझना, सिर्फ individual technologies नहीं, ऐसी capabilities को explain करता है जो कोई single system provide नहीं कर सकता। 10-minute का loan, instant identity verification, paperless document sharing, ये सब layers की interaction से emerge होते हैं। भारत ने कुछ genuinely नया बनाया है: population-scale digital infrastructure जो public goods के रूप में operate होता है।

Living traditions

India Stack देश का 21st century में global technology governance के लिए सबसे significant contribution है। यह prove करके कि population-scale DPI संभव है, और designs को open-source करके, भारत ने influenced किया है कि दुनिया digital infrastructure के बारे में कैसे सोचती है। India Stack में embedded principles, interoperability, consent, state-as-platform, global standards बन रहे हैं।

- हर जगह आधार eKYC: Bank account खोलना, SIM card लेना, mutual fund investments शुरू करना, सब कुछ अब आधार eKYC के ज़रिए कुछ मिनटों में होता है। जो पहले multiple documents और branch visits require करता था, अब सिर्फ fingerprint या OTP authentication चाहिए।

- डॉक्यूमेंट्स के लिए DigiLocker: आपका driving license, vehicle registration, educational certificates, और vaccine records DigiLocker में available हैं। Increasingly, institutions physical documents की जगह DigiLocker links को accept करते हैं, paperless verification को enable करते हुए।

- Account Aggregator सहमति Dashboards: बहुत सारे banks अब consent dashboards offer करते हैं जो दिखाते हैं कि कौन सा डेटा Account Aggregator के ज़रिए share हुआ है, किसके साथ, और कितने समय के लिए। अपने bank के app में 'AA' या 'consent' section check करें अपना data sharing history देखने के लिए।

- iSPIRT Foundation, बेंगलुरु: यह non-profit think tank है जिसने India Stack architecture का बहुत कुछ design किया। हालांकि यह एक tourist destination नहीं है, iSPIRT occasionally public events host करता है और इसे 'garage' कहा गया है जहां भारत का digital infrastructure design हुआ था।

- UIDAI Regional Offices: आधार के पीछे की organization के regional offices हैं जहां आप enrollment और authentication operations को see कर सकते हैं। कुछ offices educational tours offer करते हैं जो दिखाते हैं कि दुनिया का सबसे बड़ा biometric database कैसे operate होता है।

- रामेश्वरम् मंदिर ट्रस्ट: यह ancient temple pilgrim management के लिए India Stack का use करता है, services के लिए आधार verification, donations के लिए यूपीआई, और sacred water ceremony (Tirtha) के लिए digital records

- जगन्नाथ मंदिर: यह famous Rath Yatra temple prasad booking, accommodation management, और donation tracking के लिए India Stack को integrate किया है, pilgrimage administration को modernize करते हुए

Reflection

- India Stack बहुत सारी services को faster और ज़्यादा accessible बनाता है, लेकिन यह unprecedented data trails भी create करता है। हर आधार authentication, हर यूपीआई transaction, हर AA consent record होता है। क्या यह trade-off (convenience के बदले में data creation) worth है? इन data trails से कौन benefit करता है, आप, institutions, या दोनों? क्या किए हुए करने से बचाने के लिए कौन से guardrails exist होने चाहिए?

- एक हफ्ते के लिए अपने 'India Stack touchpoints' को map करें। हर बार जब आप आधार use करते हैं (authentication, eKYC), यूपीआई, DigiLocker, या Account Aggregator को encounter करते हैं, इसे note करें। हफ्ते के आखिर में, count करें: आपने stack से कितनी बार interact किया? किस layer का आपने सबसे ज़्यादा use किया? क्या कोई friction points थे? कोई moments जहां आप surprised थे कि सब कुछ कितनी seamlessly काम कर रहा था?