Sahakari: The Cooperative Movement in India

Banking by the People, for the People

When moneylenders charged 40% interest and banks ignored villages, farmers built their own banks. The cooperative movement, sahakari, transformed ancient principles of mutual aid into India's largest rural financial network. This lesson traces how Dharmashastra's cooperative ethics met German credit union models to create a uniquely Indian financial institution serving 130 million members.

The Meeting That Saved a Village

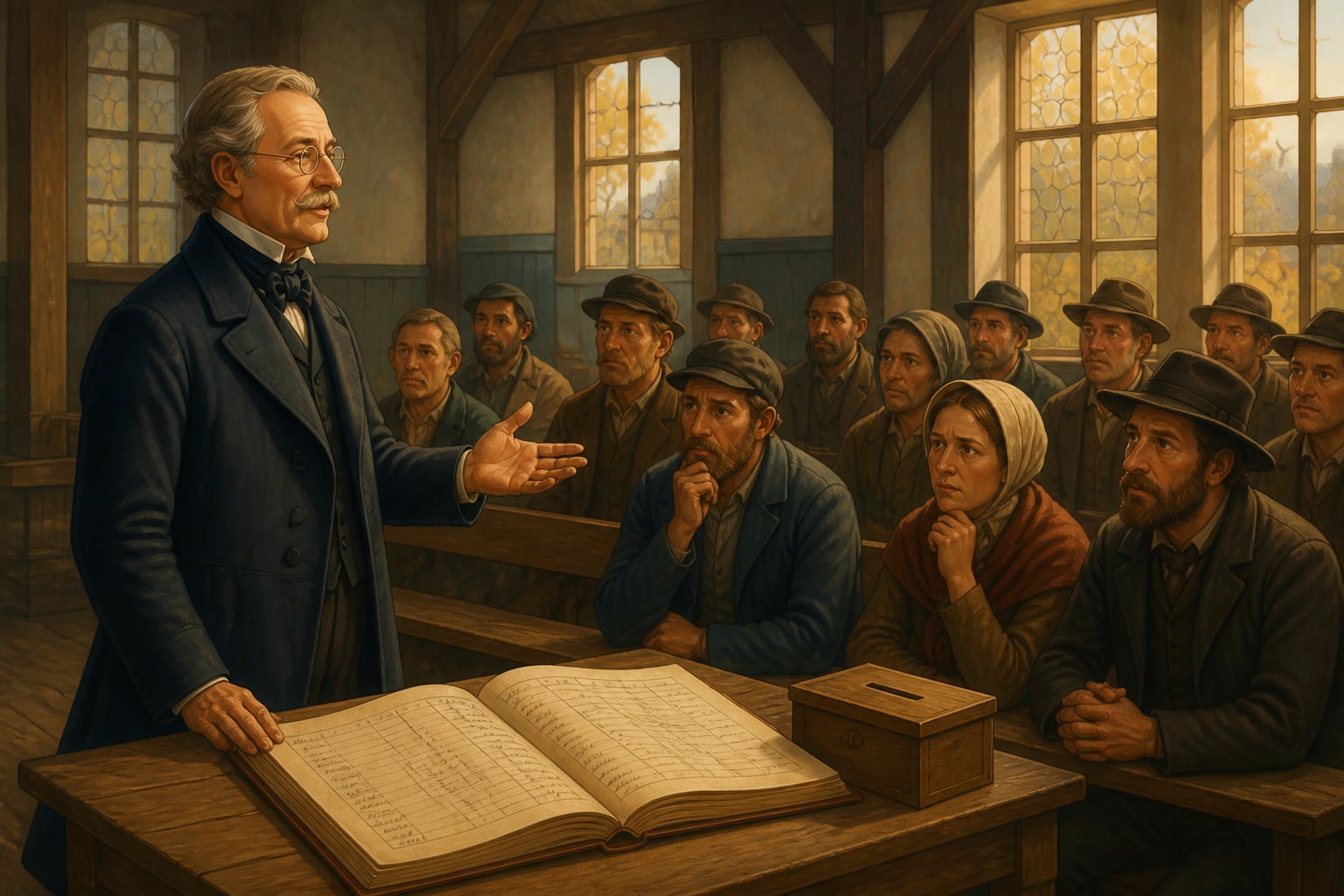

In 1907, the farmers of Kanaginahal village in Karnataka faced extinction. Three consecutive crop failures had pushed every family into debt to local moneylenders charging 36-60% annual interest. Land was being seized. Farmers were committing suicide. The village temple, which had served as an informal lending institution for centuries, had exhausted its funds.

Then the District Collector arrived with an unusual proposal. He had read the report of Frederick Nicholson, a British officer who had studied both German credit cooperatives and Indian village traditions. His conclusion: India already had the cooperative instinct, it just needed a legal structure.

Twenty-three farmers gathered that evening. They pooled their remaining savings, ₹57 total, and registered as the Kanaginahal Cooperative Credit Society. Within five years, every moneylender had left the village. Within a decade, land seizures had stopped entirely.

This wasn't a foreign import. It was the formalization of something Indians had practiced for millennia.

The Ancient Roots of Sahakara

The Sanskrit term sahakara (सहकार) literally means "working together", from saha (together) and kara (doing). But cooperation in Indian tradition wasn't merely practical; it was dharmic.

The Narada Smriti, a Dharmashastra text from approximately 100-400 CE, provides explicit legal frameworks for collective enterprises:

सहकार्यं समानानां समानार्थसमागमः

Sahakāryaṃ samānānāṃ samānārthasamāgamaḥ

"Cooperative action is the coming together of equals for common purpose."

This verse establishes the essential principle: cooperation is between equals (samana) for shared benefit (samanārtha). Unlike charity or patronage, sahakara implies mutual stake and mutual gain.

The Dharmashastra texts elaborated extensive rules for cooperative enterprises:

- Decision-making: Majority vote, but with provisions for consensus on major issues

- Profit distribution: Proportional to contribution or risk

- Liability: Collective responsibility, but limited to contributed amounts

- Dissolution: Fair distribution of assets based on contribution and tenure

- Expulsion: Possible for breach of collective agreements, but with due process

The medieval merchant guilds (shreni) we encountered in our chitty lesson implemented these principles on a massive scale. The Manigramam and Nanadesi guilds operated credit facilities, insurance pools, and collective investment funds, essentially cooperative banks without the modern terminology.

The Yajnavalkya Smriti adds an ethical dimension:

अन्योन्यं परिरक्षन्तः कुलान्यात्मानमेव च

Anyonyaṃ parirakṣantaḥ kulānyātmānameva ca

"Protecting each other, families protect themselves."

This encapsulates the cooperative insight: collective security enhances individual security. It's not sacrifice for the group, it's enlightened self-interest organized collectively.

The German Connection: Raiffeisen's Credit Unions

While India had cooperative traditions, the modern cooperative movement emerged from a different crisis in a different land.

In 1846, Friedrich Wilhelm Raiffeisen (1818-1888), the mayor of a small German town, watched his farmers starve after a crop failure. Moneylenders offered loans at usurious rates. Banks existed only in cities. Raiffeisen had an insight: if the farmers pooled their savings and lent to each other, they could eliminate the middleman.

He created the first Darlehnskassen-Verein (credit union) in 1864 with these principles:

- Unlimited liability: Members were collectively responsible for all debts (ensuring careful lending)

- No share capital: The union was built on trust, not investor capital

- Geographic limitation: Only neighbors could join (ensuring local knowledge)

- Voluntary service: Directors served without pay (keeping costs low)

- Surplus for reserves: Profits built community capital, not dividends

By 1888, there were 425 Raiffeisen banks across Germany, transforming rural finance.

Frederick Nicholson, a British colonial officer in Madras Presidency, studied the Raiffeisen model in 1895. His landmark report concluded: "Find Raiffeisen!", meaning, replicate this model in India. But Nicholson also observed that India already had cooperative practices; what was lacking was legal recognition and formal structure.

The Cooperative Credit Societies Act of 1904 was the result, the legal foundation that allowed village cooperatives like Kanaginahal to register, operate bank accounts, and enforce contracts.

| Feature | Raiffeisen Model | Indian Adaptation |

|---|---|---|

| Liability | Unlimited | Modified to limited (protecting small farmers) |

| Geography | Village-based | Village-based (matching panchayat structure) |

| Governance | Elected board | Elected board with government oversight |

| Purpose | Credit only | Credit + savings + input supply |

| Culture base | Christian mutual aid | Dharmic sahakara principles |

The Architecture of Indian Cooperatives

India's cooperative structure evolved into a three-tier pyramid:

Tier 1: Primary Agricultural Credit Societies (PACS)

- Village-level, member-owned

- ~95,000 societies across India

- 13+ crore member families

- Provide short-term crop loans, input supplies, storage

Tier 2: District Central Cooperative Banks (DCCBs)

- District-level, owned by PACS

- ~350 banks

- Channel funds from state to village level

- Provide medium-term loans for equipment, wells

Tier 3: State Cooperative Banks (SCBs)

- State-level apex institutions

- ~33 banks

- Interface with RBI and NABARD

- Provide long-term loans for land development

This structure allows village-level operations while aggregating capital at scale. A farmer in a remote village can access institutional credit through a chain that connects their local PACS to national financial infrastructure.

The Creation of the Cooperation Ministry: 2021

In July 2021, the Government of India created a historic new institution: the Ministry of Cooperation, with Amit Shah as its first minister. This elevated cooperation from a subject handled by various departments to a full-fledged ministry, the first such ministry in independent India.

The timing wasn't accidental. India's cooperative sector had grown to:

- 8.5 lakh+ cooperatives across sectors (credit, dairy, housing, consumer, labor)

- 30+ crore members (including families, 100+ crore people touched)

- ₹30+ lakh crore in assets

- The world's largest cooperative network by membership

Yet the sector faced challenges: governance issues in some state cooperative banks, technology gaps at the village level, and inconsistent regulation across states. The new ministry aimed to address these while expanding the model.

Key initiatives since 2021:

- PACS Computerization: Connecting all 95,000 PACS to a national digital platform

- Multi-purpose PACS: Expanding from credit to include gas distribution, water supply, seeds, fertilizers

- Model Bylaws: Standardizing governance across states

- Cooperative University: Training professional managers for cooperatives

- PACS as CSCs: Converting Primary Agricultural Credit Societies into Common Service Centers for government services

The vision: transform cooperatives from credit-focused institutions into "one-stop shops" for rural services, essentially, making the village cooperative the Amazon of rural India, owned by the villagers themselves.

Global Perspectives: Cooperation Worldwide

The cooperative model has achieved remarkable scale globally, validating the Indian insight that communities can organize economic life effectively.

International Cooperative Alliance (ICA) data shows:

- 3 million+ cooperatives worldwide

- 1 billion+ members (1 in 7 humans)

- 280 million+ jobs (10% of global employment)

- Top 300 cooperatives: $2.2 trillion turnover (larger than India's GDP)

Notable global examples:

| Country | Cooperative Sector | Scale |

|---|---|---|

| Germany | Raiffeisen banks | 18.5 million members, €200B+ assets |

| Japan | JA (Agricultural) | 10 million farmer members, controls rice distribution |

| Spain | Mondragon | 80,000 worker-owners, €12B revenue |

| Kenya | Savings cooperatives | 14 million members (30% of population) |

| India | PACS + all cooperatives | 30+ crore members, largest by membership |

What distinguishes India's approach:

- Scale: No country has achieved India's depth of cooperative penetration in villages

- Government partnership: India uses cooperatives as policy delivery mechanisms (MSP procurement, input distribution)

- Multi-sector integration: The same PACS can handle credit, dairy collection, and fertilizer supply

- Constitutional status: Cooperatives are mentioned in the Constitution (Article 43B) as a policy directive

Modern Resonance: PACS in the Digital Age

In 2024, Kamala Devi, a farmer in Rajasthan's Jhunjhunu district, opens her phone. She's checking her PACS account balance, something impossible two years ago. Her local PACS, Khemi Ki Dhani, is now connected to the national PACS digitization platform.

This morning, she:

- Applied for a crop loan (processed in 2 days instead of 2 weeks)

- Purchased subsidized seeds through the PACS e-commerce platform

- Scheduled her LPG cylinder delivery (PACS as CSC)

- Paid her electricity bill

"Earlier, I went to the district town for all this," she explains. "Now my PACS is everything, bank, shop, government office."

The transformation is still incomplete. Only about 30,000 of 95,000 PACS are fully digitized. But the vision is clear: the village cooperative as digital infrastructure, combining ancient sahakara principles with modern technology.

Data point: In 2023-24, PACS disbursed over ₹1.5 lakh crore in agricultural credit, more than many commercial banks' rural lending combined.

Your Turn: The Cooperative Instinct

You likely participate in cooperative structures without realizing it:

- Housing societies: Most urban apartment buildings are registered cooperatives

- Credit unions: Many employee welfare funds operate cooperatively

- Consumer cooperatives: Kendriya Bhandar, Apna Bazaar, Mother Dairy

- Producer organizations: Farmer Producer Organizations (FPOs) are cooperatives by another name

The cooperative principle applies beyond formal registration:

- Carpooling: Sharing costs of transportation collectively

- Group buying: Negotiating bulk discounts together

- Community support: WhatsApp groups that share resources and information

The question isn't whether you'll encounter cooperatives, you already do. The question is: Could you organize cooperative solutions for problems in your life?

A neighborhood could form a cooperative for solar power. A professional community could create a cooperative for health insurance. A group of freelancers could form a cooperative for shared office space and marketing.

The Dharmashastra principles remain valid: sahakāryaṃ samānānāṃ, cooperation is equals coming together. In our next lesson, we'll explore how women took this principle and created India's most successful grassroots financial revolution: the Self-Help Group movement.

Modern insurance theory, from Lloyd's of London (1686) to contemporary actuarial science, is based on the same principle: aggregating many independent risks creates predictable outcomes. The law of large numbers makes collective risk-sharing mathematically optimal.

India's cooperative insurance system, including crop insurance delivered through PACS and life insurance through cooperative insurers like LIC, reaches populations that private insurers avoid. The sahakara principle enables coverage where profit-driven models fail.

Pradhan Mantri Fasal Bima Yojana (crop insurance) covers 5+ crore farmers annually, largely delivered through PACS networks, the world's largest agricultural insurance program.

In corporate governance, voting power typically follows capital: one share, one vote. This makes shareholders-as-owners the governing principle. Cooperatives invert this: one member, one vote, regardless of capital. The Rochdale Pioneers (1844) formalized this, but the Dharmashastra anticipated it.

Democratic governance ensures cooperatives serve member needs, not investor returns. When every farmer has equal voice, the cooperative can't prioritize large landowners over small ones. This is why PACS remain relevant to marginal farmers whom commercial banks ignore.

Of India's 13+ crore PACS members, over 50% are marginal farmers (less than 1 hectare). Democratic governance ensures their voice isn't drowned by larger farmers.

Key terms

- Sahakara

- Cooperation, working together, the principle of collective action for mutual benefit. In modern usage, refers to the cooperative movement and cooperative enterprises.

- Prathamik Krishi Sakh Samiti (PACS)

- Primary Agricultural Credit Society, the village-level cooperative that provides credit, inputs, and services to farmer members. The foundation of India's three-tier cooperative credit structure.

- Sadasyata

- Membership, the status of being a member-owner in a cooperative, with rights to vote, access services, and share in surpluses.

- Adhishesha

- Surplus, the excess of income over expenses in a cooperative, distributed to members or retained for collective benefit. Cooperatives speak of 'surplus' rather than 'profit' to emphasize the non-commercial nature.

Key figures

Dharmashastra Tradition (Narada, Yajnavalkya, Brihaspati)

Established the dharmic foundations of cooperation: equality among members, collective decision-making, proportional distribution, and mutual protection. These principles predated European cooperative theory by over a thousand years and provided the cultural substrate that made Indian villages receptive to formal cooperative structures in the 20th century.

Amit Shah (as Cooperation Minister)

Driving the digitization of 95,000+ PACS, transforming them into multi-service delivery platforms. Key initiatives include computerization of all PACS by 2025, enabling them as Common Service Centers, standardizing governance through Model Bylaws, and expanding cooperative credit through the ₹2,500 crore Computer-based Cooperative Societies (CSS) scheme.

Friedrich Wilhelm Raiffeisen

Created a replicable model for transforming village-level mutual aid into formal financial institutions. The Raiffeisen principles, geographic limitation (only neighbors can join), character-based lending (local knowledge replaces credit scores), and member governance, directly influenced India's Cooperative Credit Societies Act of 1904.

Case studies

PACS Transformation: From Credit Society to Rural Service Center

In 2022, the Sardargarh PACS in Rajasthan's Churu district was a typical village cooperative: a single-room office with paper ledgers, one part-time employee, and a narrow focus on crop loans. It served 850 member families with annual credit disbursement of about ₹2 crore. Then it was selected for the Ministry of Cooperation's computerization pilot. Within 18 months: 1. **Digital infrastructure**: Computer, internet, biometric devices, and software connected to state cooperative bank 2. **Expanded services**: Beyond credit, LPG booking, electricity bill payment, Aadhaar-enabled services, government scheme enrollment 3. **New revenue streams**: Commission from service delivery (₹15-50 per transaction) 4. **Staff upgrade**: Two full-time trained employees replacing one part-time 5. **Banking correspondent**: Partnership with State Bank of India for basic banking services The PACS now processes 200+ transactions daily versus 5-10 previously. Loan processing time dropped from 2 weeks to 3 days. Member families visit the PACS weekly instead of twice yearly.

The transformation embodies the Dharmashastra concept of sangha as comprehensive community institution, not just a single-purpose entity but a center of collective life. The PACS evolution from credit-only to multi-service mirrors the ancient guild model where shrenis provided credit, insurance, arbitration, and community services. Critically, the cooperative structure ensures that service expansion benefits members, not external shareholders. When Sardargarh PACS earns commission from LPG bookings, that surplus flows to the community, either as lower loan rates, higher deposit rates, or retained capital for expansion. This is dharmic economics in practice: using collective organization to capture value for the community rather than extracting it.

By 2024, Sardargarh PACS metrics showed: - **Credit disbursement**: Up 150% to ₹5 crore (more families accessing formal credit) - **Non-credit transactions**: 3,000+ monthly (government services, bill payments, banking) - **Member engagement**: 70%+ of member families using services monthly (up from <30%) - **Staff income**: Full-time employees earning ₹15,000+/month (formal employment in the village) - **Model replication**: Selected as training site for other PACS in the district The Ministry aims to replicate this across 95,000 PACS by 2025, a transformation that would make cooperatives India's largest rural service delivery network.

Cooperatives can evolve from narrow-purpose organizations to comprehensive community infrastructure. The digital transformation of PACS shows that traditional institutions, when upgraded with technology and expanded scope, can serve needs that neither government offices nor private businesses efficiently address. The key: member ownership ensures the institution serves the community, not external interests.

India's PACS digitization initiative could create the world's largest village-level financial network. This mirrors how China's rural cooperative credit system was digitized in the 2010s, which now processes trillions of yuan annually and serves as the backbone of rural Chinese finance.

The ₹2,516 crore PACS computerization scheme aims to connect all 95,000 PACS by 2025. If achieved, India will have the world's largest digitally-connected network of village-level financial institutions.

The Three-Tier System in Action: Flood Relief Credit in Bihar

In August 2023, severe floods in Bihar's Darbhanga district devastated the kharif crop for 150,000 farming families. Commercial banks, citing damaged collateral and uncertain repayment, largely withdrew from lending. Moneylenders arrived offering loans at 60% annual interest. The cooperative credit system activated its three-tier response: **Tier 1 - PACS Level (450 village societies):** - Immediate moratorium on existing loan repayments - Emergency consumption loans (₹10,000-25,000) within 48 hours - No fresh collateral required, member history sufficient - Interest rate: 7% (versus 60% from moneylenders) **Tier 2 - DCCB Level (Darbhanga District Central Cooperative Bank):** - Channeled ₹150 crore emergency credit line to PACS - Coordinated assessment of damage across societies - Standardized documentation for crop insurance claims **Tier 3 - SCB Level (Bihar State Cooperative Bank):** - Arranged refinance from NABARD at concessional rates - Interfaced with state government for interest subvention - Coordinated with crop insurance company for claims processing Within 60 days, 80,000+ families received emergency credit through their local PACS, without leaving their village.

The flood response demonstrates the Yajnavalkya Smriti's principle in action: 'Protecting each other, families protect themselves.' The three-tier system creates a cascade of mutual protection: - PACS members protect each other through collective creditworthiness - PACS are protected by DCCB coordination and capital - DCCBs are protected by SCB refinancing - SCBs are protected by NABARD and state government backup No individual farmer could have accessed ₹150 crore in emergency credit. But organized collectively through cooperatives, each family accessed what they needed. This is sahakara at scale, the village-level principle extended through institutional architecture. Commercial banks, by contrast, retreated because their model depends on individual collateral and credit scoring, mechanisms that fail precisely when they're most needed (during crises).

The Bihar cooperative response achieved: - **Speed**: Average 5 days from application to disbursement (versus 30+ days for commercial banks) - **Coverage**: 80,000+ families served (commercial banks served <10,000) - **Cost**: 7% interest (versus 40-60% from moneylenders) - **Recovery**: 85%+ repayment rate in subsequent year (trust-based lending worked) - **Systemic**: No farmer suicides reported in covered areas (versus 12 in areas without cooperative coverage) The episode validated why India maintains a parallel cooperative credit system despite commercial bank expansion: in crises, member-owned institutions don't flee.

The cooperative system's value is clearest in crises. When commercial logic says 'retreat' (high risk, uncertain returns), cooperative logic says 'protect members' (shared fate, mutual obligation). This counter-cyclical behavior, lending more when times are worst, is only possible because cooperatives are owned by the borrowers themselves.

Climate disasters are increasing globally, and commercial banks consistently retreat from affected areas. The cooperative credit model's ability to maintain lending during crises is attracting attention from climate adaptation planners who recognize that financial resilience must be built before disasters strike.

In 2023-24, cooperative credit societies (PACS + DCCBs) disbursed ₹1.5+ lakh crore in agricultural credit, approximately 20% of total agricultural lending in India, but over 50% in flood/drought affected areas.

Historical context

Ancient Period to Present

India's cooperative movement emerged from the collision of three forces: ancient traditions of mutual aid (documented in Dharmashastra), colonial crisis (moneylender exploitation following land revenue demands), and imported institutional models (German credit unions via British administrators). The result was a unique hybrid: German structure with Indian cultural roots, serving populations that neither indigenous informal finance nor colonial banking could reach.

India has the world's largest cooperative sector by membership (30+ crore members) but not by assets or efficiency. German cooperative banks are far more professionally managed; Japanese agricultural cooperatives have greater market power; Mondragon in Spain demonstrates industrial-scale worker ownership. India's challenge is upgrading governance and technology while preserving the democratic, member-serving character that makes cooperatives valuable.

The cooperative sector contributes approximately 3% to India's GDP directly, but its indirect impact, through agricultural credit, input supply, and market linkage, affects 60%+ of rural economic activity.

Understanding the cooperative system reveals an alternative to the binary of 'government provision vs. private market.' Cooperatives represent a third way: member-owned, community-governed institutions that combine collective action with local accountability. In an era of debates about financial inclusion and rural development, the cooperative model offers tested solutions.

Living traditions

The cooperative model continues to evolve. PACS are being transformed into digital service centers. Farmer Producer Organizations (FPOs), essentially marketing cooperatives, are growing rapidly under government promotion. Housing cooperatives remain the dominant form of urban apartment ownership. The Ministry of Cooperation's vision of multi-purpose PACS as 'one-stop shops' represents the latest iteration of the ancient sahakara principle: community institutions that serve comprehensive member needs.

- Village Loan Committee Meetings: PACS hold regular committee meetings where members discuss loan applications, review repayments, and make collective decisions about credit allocation. These meetings embody the democratic governance principle, every member's voice counts.

- Annual General Meetings: Cooperative law requires annual meetings where all members can vote on accounts, elect boards, and question management. These AGMs, often the largest gatherings in village calendars, are the operational expression of democratic ownership.

- Cooperative Day Celebrations: July 6 is observed as International Cooperative Day. In India, PACS and other cooperatives organize events highlighting member achievements, distributing surplus, and recognizing long-standing members.

- National Cooperative Union of India (NCUI), New Delhi: The apex organization of India's cooperative movement, housing archives of cooperative history, training facilities, and the Cooperative Museum documenting the movement's evolution from 1904 to present.

- Kanaginahal Village, Karnataka: Site of one of India's earliest successful credit cooperatives (1907). The village remains a model of cooperative-led development, with multiple cooperative institutions serving different needs.

- Institute of Cooperative Management (ICM) Network: Training institutes in multiple states where cooperative managers are professionally trained. Visitors can observe how traditional cooperative principles are being combined with modern management techniques.

- Dharmasthala Temple Complex: This temple complex runs one of India's most successful cooperative-style microfinance programs, providing interest-free loans to thousands; demonstrates the temple as a center of ethical community finance

- Vitthal Temple: The warkari tradition associated with this temple emphasizes community cooperation and collective welfare, principles that influenced the cooperative movement in Maharashtra

Reflection

- The cooperative principle assumes that 'equals coming together for common purpose' will produce better outcomes than hierarchical organization or pure market competition. In your experience, when does collective organization work well, and when does it fail? What conditions make the difference between successful cooperation and dysfunctional committees?

- Identify a problem in your community or professional network that might benefit from cooperative organization: perhaps group health insurance, shared workspace, collective purchasing, or mutual professional support. Design a basic cooperative structure: Who would be members? What would the governance look like? How would costs and benefits be shared? What would make it succeed or fail?